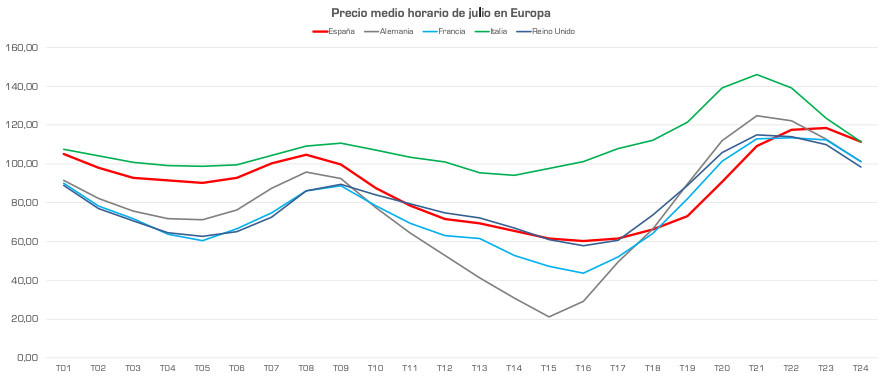

Prices have plummeted in Germany during the central hours of the day. Many days have registered negative prices due to the combination of low demand and high solar generation during those hours. In fact, on July 2nd, negative prices in the Netherlands, Germany, and Austria reached -€500/MWh, the minimum according to European Union regulations.

Although this is not a new phenomenon, its scope and duration are indeed increasing, highlighting the growing demand flexibility deficit in Europe. In Germany, the lack of flexibility in its coal fleet and the high installed solar capacity (58.9 GW) pose a challenge to its electrical system.

Negative prices are not allowed in Spain, and we have also not seen “zero” prices in July. High temperatures in our country lead to an increase in demand during the central hours, which can be 30% higher than during the same time span in spring, which “neutralises” the strong solar generation. Indeed, it is in spring when the most favourable weather conditions in Spain are seen for “zero” prices, which we have already seen in April and May.

Electricity generation drops by 10% and photovoltaic grows by 32%

This month, photovoltaic generation has been 32% higher than a year ago and has taken the third position in the mix, after nuclear and combined cycles. In contrast, wind generation has decreased by 13%.

Total electricity generation has been 10% lower due to the significant reduction in exports (-78.3%) and the drop in demand (-3.8%). As we pointed out in our fortnightly advance, the disappearance of the gas price cap and the increase in French nuclear production have led to a shift in the balance with our French neighbours from exporter to importer.

Combined cycle gas (CCG) plants have seen the greatest reduction in their production (-42.5%). Despite this, the CCGs have occupied the second position in the mix, contributing 19.5%, only lower than nuclear (20%). The significant presence of CCGs during the central hours of the day, due to lower wind generation, has prevented the price of electricity from falling further in July.